Analyzing Financial Statements: The Horizontal Method

The second method to analyze financial statements is the horizontal method. The horizontal method is used to analyze financial information in two fiscal years.

This method consists of comparing various financial statements, and it has a comparative evaluation between two years as less to identify the evolution of different accounts.

The method involves increasing and decreasing, a technique used to compare similar concepts on different dates. The object is to locate differences or inconsistent and analyze the accounts’ behavior year by year.

We determine if the variation is positive (increase) or negative (decrease).

To ensure a good analyze we recommend following the following steps:

Step #1

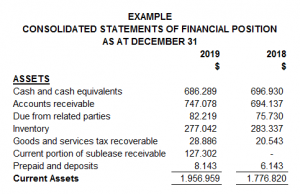

Having the financial statements in an Excel format will make it easier for the necessary calculations. Make sure you include the complete accounts next to their amounts and the two years correspondence. In the following example, we can see how it must look.

|

Step #2

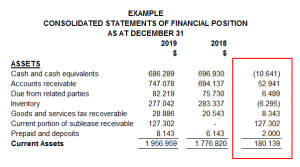

Include two columns next to the amounts inserted; the first one will be used to present the increases and decreases, and the second one will show the percentages.

The horizontal method takes each account’s value from the last year minus each account’s worth from the previous year.

For example, cash and cash equivalents from 2019 minus cash and its equivalents from 2018, as we can see as follow:

|

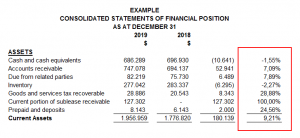

Then, the result is divided by the total of the account from the last year. In this case, the result was divided by the total cash and cash equivalent from 2019 (the most recent year), obtaining 1.55%.

|

Step #3

Once the percentages have been obtained, the user of the financial statements can select the account with more variation (a positive percentage if the account had an increase or a negative percentage if the account had a decrease) in the assets, liabilities, or income loss statement.

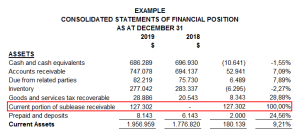

In the following example, we have the current portion of sublease receivable with 100% positive variation and cash and cash equivalents with 1.55% negative variation. The first have our special attention because it has more than 50%.

|

Step #4

The analyst can start making questions about the variations; the first one could be which sublease did the company celebrate? In which operations or inversions the company expended cash?

You could have that information having an interview with the accounting department, the administrator, or even directly with the company’s owner, also. If the financial statement has been audited, you could read its notes.

With this method and the vertical method, it is essential to be sure about the accounts you are reviewing and investigate a lot about them. Make questions, look for supporting documents and call an expert if necessary.

Written by: Andrea Diaz

Related Articles:

Newsletters

Newsletter – March 2019

NewslettersEvents & SponsorshipArticles & Publications

Newsletter – February 2019

NewslettersEvents & SponsorshipArticles & Publications

Newsletter December 2018

NewslettersEvents & SponsorshipArticles & Publications

Newsletter November 2018

NewslettersEvents & SponsorshipArticles & Publications

e-Newsletter – August 2018

NewslettersEvents & SponsorshipArticles & Publications

Events & Sponsorship

No Results Found

The page you requested could not be found. Try refining your search, or use the navigation above to locate the post.

Articles & Publications

RRSP/RRIF and non-registered investments

Drawing from your RRSP/RRIF and non-registered investments. It often helps to think in terms of family wealth and tax efficiency. One of the most asked questions the newly retired or those about to retire have is: "When should I start drawing from my registered...

Strategies to consider when buying a second property

Strategies to consider when buying a second property. There are three common types of second properties people are looking at when they wish to buy a second property: cottages, income properties and U.S. real estate. COTTAGE PROPERTIES If you've been looking to buy a...

Incorporating your Business in Canada

Tax Advantages of Incorporating your Business in Canada Incorporating your business may lead to lower taxes depending on your particular situation and the province in which you operate. Incorporating can save you money once the business generates more income than you...

How much is child benefit in Canada per month?

How much is child benefit in Canada per month? For each child: under six years of age: $6,833 per year ($569.41 per month) 6 to 17 years of age: $5,765 per year ($480.41 per month). Will child benefit increase in 2021? On July 20, the Minister of Families, Children...

Is Cryptocurrency Taxable in Canada?

Is cryptocurrency taxable in Canada? According to CRA, possessing or holding a cryptocurrency is not taxable. However, selling, making a gift, trading or exchanging a cryptocurrency, including disposing of one to get another, or converting cryptocurrency to a...